09.10.2020

How much risk is priced-in ahead of the US election?

There is no doubt that a US presidential election represents a risk for financial markets and a good way to quantify how much risk is currently priced-in is to look at the forward implied volatility before and after the elections.

For that, the VIX index, a basket of the S&P 500 options volatility, sounds a good barometer.

Looking at the VIX curve, The November expiry is currently trading 1.5% above the December one, reflecting the immediate risk investors are facing post-election (November 3rd) relative to December.

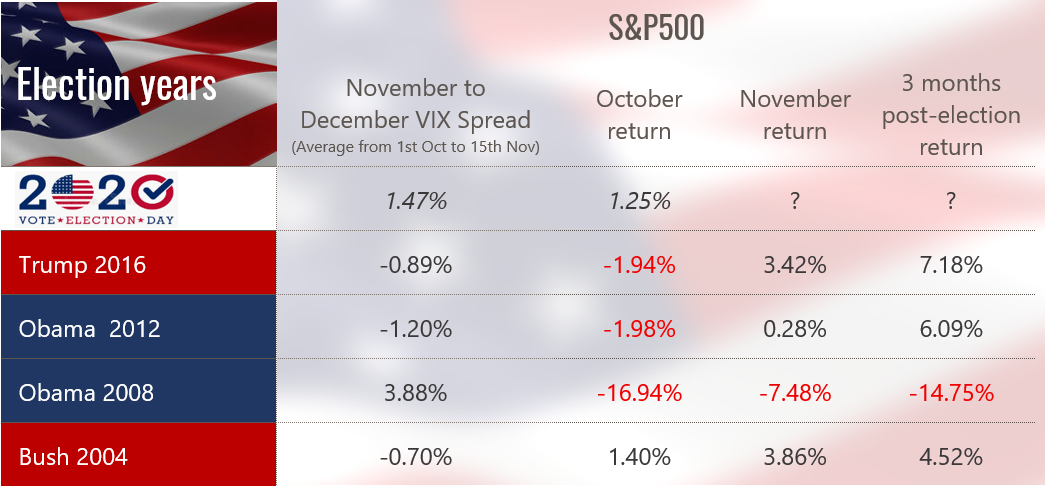

While the 1.5% spread indicates a higher implied risk around and after the election, it does not quantify the absolute level of risk. To put it in perspective, we looked at the average November-December VIX Spread from October 1st to November 15th for every US Election since 2004.

Excluding the US election during the Great Financial Crisis in 2008 where spot volatility was structurally higher than 1, 2 and 3 months forward, it appears that a positive November/December VIX Spread is somewhat unusual. In fact, during the 2004, 2012 and 2016 elections, the November VIX never traded above the December one.

Looking at the return of the S&P in October, November and 3 months after the election, we can observe that it is very difficult to draw any conclusion over a US presidential election from a financial market perspective. If anything and excluding the 2008 election during the crisis, the simple and most direct conclusion would be that a US presidential election after 2000 had a positive impact on the S&P 500 Index one month and 3 months after the outcome.

So how to explain this extra-risk this time? We believe the 1.5% premium in November volatility relative to December likely reflects one single risk: if Biden wins, President Trump might not going to accept it. A sentiment that has been reinforced after the first TV debate of the US elections.

To conclude, history shows that financial markets can easily deal with a republican or democrat president but definitely not with no President after November 4th.

More articles

24.07.2026

What if Germany were finally waking up?

If Berlin finally turns its promises into concrete projects, Germany could once again become Europe's economic engine as early as 2027.

Read more07.07.2026

Welcome to Vincent Lecoultre!

We are pleased to announce the arrival of Vincent Lecoultre as a Banker at Cité Gestion.

Read more30.06.2026

Why could the decline in oil prices reshape the investment landscape over the coming months?

La baisse des cours du pétrole pourrait modifier les perspectives d'investissement de multiples façons.

Read more23.06.2026

Crête Equestrian Competition x Cité Gestion

We are proud to have supported the Crête Horse Competition, an exceptional event that brings together passion, excellence, and camaraderie around values that are dear to us.

Read more18.06.2026

Naïma Karamoko x Cité Gestion

Cité Gestion is proud to announce its sponsorship of Naïma Karamoko and to support her promising journey, marked by her recent qualification for the WTA 125 Modena final.

Read more09.06.2026

How much is the SpaceX dream actually worth?

SpaceX’s $1.75 trillion valuation is ultimately a bet that the company can sustain near-flawless execution and technological leadership for 15 years, transforming today’s $20 billion in revenue into $3.4 trillion by 2040—a reflection of how much investors are willing to pay for a bold vision of the future.

Read more