09.10.2020

US-Wahlen: Welche Risiken sind bereits eingepreist?

There is no doubt that a US presidential election represents a risk for financial markets and a good way to quantify how much risk is currently priced-in is to look at the forward implied volatility before and after the elections.

For that, the VIX index, a basket of the S&P 500 options volatility, sounds a good barometer.

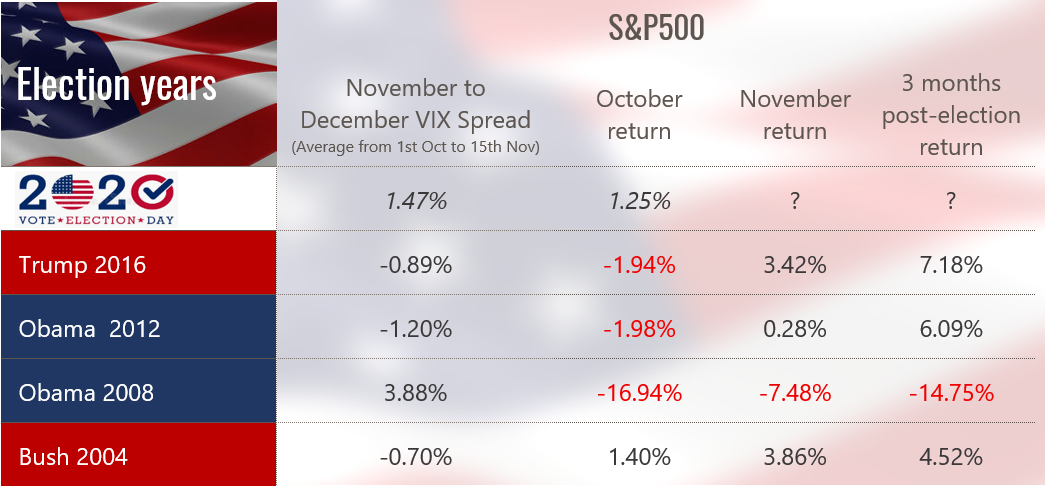

Looking at the VIX curve, The November expiry is currently trading 1.5% above the December one, reflecting the immediate risk investors are facing post-election (November 3rd) relative to December.

While the 1.5% spread indicates a higher implied risk around and after the election, it does not quantify the absolute level of risk. To put it in perspective, we looked at the average November-December VIX Spread from October 1st to November 15th for every US Election since 2004.

Excluding the US election during the Great Financial Crisis in 2008 where spot volatility was structurally higher than 1, 2 and 3 months forward, it appears that a positive November/December VIX Spread is somewhat unusual. In fact, during the 2004, 2012 and 2016 elections, the November VIX never traded above the December one.

Looking at the return of the S&P in October, November and 3 months after the election, we can observe that it is very difficult to draw any conclusion over a US presidential election from a financial market perspective. If anything and excluding the 2008 election during the crisis, the simple and most direct conclusion would be that a US presidential election after 2000 had a positive impact on the S&P 500 Index one month and 3 months after the outcome.

So how to explain this extra-risk this time? We believe the 1.5% premium in November volatility relative to December likely reflects one single risk: if Biden wins, President Trump might not going to accept it. A sentiment that has been reinforced after the first TV debate of the US elections.

To conclude, history shows that financial markets can easily deal with a republican or democrat president but definitely not with no President after November 4th.

Mehr Publikationen

05.08.2026

Wird die Kernenergie die Energiequelle für die KI-Revolution sein?

Die Kernenergie entwickelt sich aufgrund ihrer Fähigkeit, stabilen, grossvolumigen und kohlenstoffarmen Strom bereitzustellen, zu einem der führenden Kandidaten für die Energieversorgung der KI-Revolution.

Mehr dazu01.08.2026

Einen schönen Schweizer Nationalfeiertag!

Heute feiern wir nicht nur einen Nationalfeiertag, sondern auch die Werte, die die Schweiz seit Generationen prägen: Vertrauen, Zuverlässigkeit und Spitzenleistungen.

Bei Cité Gestion sind diese Grundsätze Teil unseres Erbes und bilden die Grundlage für unser tägliches Engagement.

24.07.2026

Was wäre, wenn Deutschland endlich aufwachen würde?

Deutschland bereits 2027 wieder zum Wirtschaftsmotor Europas werden.

Mehr dazu07.07.2026

Willkommen, Vincent Lecoultre!

Wir freuen uns, Ihnen mitteilen zu können, dass Vincent Lecoultre als Banker zu Cité Gestion gekommen ist.

Mehr dazu30.06.2026

Warum könnte der Rückgang der Ölpreise die Investitionslandschaft in den kommenden Monaten neu gestalten?

Niedrigere Ölpreise könnten die Investitionsaussichten in vielerlei Hinsicht verändern.

Mehr dazu23.06.2026

Reitturnier von Crête x Cité Gestion

Wir sind stolz darauf, das Reitturnier auf Kreta unterstützt zu haben – eine aussergewöhnliche Veranstaltung, die Leidenschaft, Spitzenleistungen und Geselligkeit vereint und dabei Werte verkörpert, die uns am Herzen liegen.

Mehr dazu