03.05.2022

In Focus: US Treasury yield curve sends mixed signals | May 2022

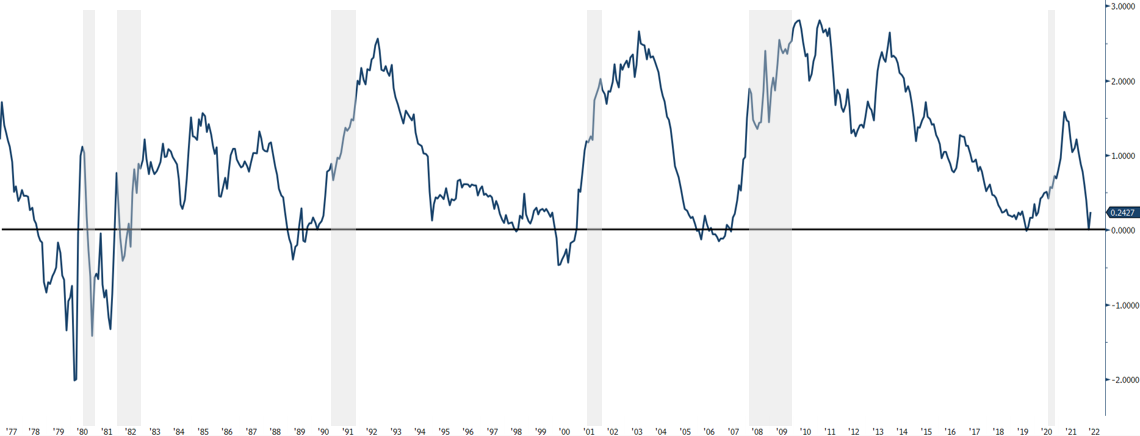

In the early days of the month of April, the closely watched 2Y/10Y yield curve has inverted multiple times over a short time span. High emphasis is put on this point of data as it has in the past often been synonymous in announcing a recession of the US economy. While many strategists explained that the rise in concern over this matter should not spark fear in the markets, others highlight putting the 2Y/10Y in correlation with the Consumer Optimism Gap clearly illustrates that a downward slopping yield curve matches a fall in consumer optimism and eventually provides fertile ground for a recession.

US 2Y/10Y - Average of 18 months from inversion to recession:

History tells us since the 1960s’ every recession where economic decline during which trade and industrial activity are reduced, generally identified by a fall in GDP in two successive quarters has only occurred after an inversion of the 2Y/10Y. Following this chain of thought, we can now suppose that additional risk is weighing in the basket in seeing a declining growth of the US economy in one to two years time.

US 2Y/10Y (blue) vs Consumer Optimism Gap (red):

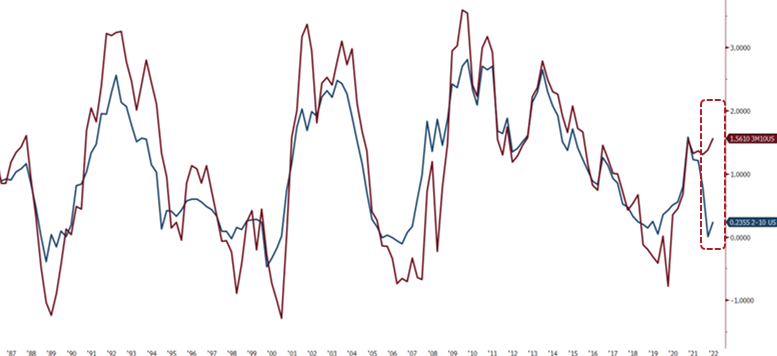

Don’t panic the 3M/10Y still remains steep

All yield curves between 2 and 10 years have inverted. Remains the 3 month, which is taking a steep route in positive territory. This phenomenon can be interpreted in two ways. The first could be a reflection of the FED being behind the curve. Something that should not last over the upcoming quarters as future hikes are on target following the rise of the 4th of May.

An upward slopping curve happens when investors require additional return on debt as they envision greater default risk of the underlying or a possible fear of inflation. The divergence between the 3M/10Y could also be a signal of increasing hawkishness from the FED in the upcoming years.

Finally, while some mention an inversion of the 2Y/10Y leaves us on average more than a year and half to face a potential recession, it is worth highlighting that a recession occurring after a 1st rate hike in a cycle happens earlier when the 2Y/10Y inversion occurs during the hiking cycle. The last inversion of March 2022 occurred in the quickest time span recorded after the start of the hiking cycle.

US 3M/10Y (red) vs 2Y/10Y (blue):

Asset class performance post-inversion

The average performance post inversion of the S&P 500 does not show cast a clear pattern. No correlation can be established between the inversion and performance of US stock index before, during and after a cycle.

We should bear in mind that short and long-term dynamics shape the yield curve. Two years ago, before the COVID-19 outbreak the FED has cut its policy rate to near zero in order to limit the impact of a recession caused by the pandemic.

Fast forward to today’s terms, the FED has to “catch up” with growing inflation as both global and US economy recovers to its pre-pandemic levels. The T-Bill is facing strong global demand combined to the FEDs’ ongoing quantitative easing (QE) that has for effect to increase prices of bonds resulting in low yields. The steepness of short-term yields has caught a great deal of attention, ultimately opening the debate of future economic outlook on either an unconventional slowdown in growth or a strong signal of a US recession; the question remains open.

More articles

07.07.2026

Welcome to Vincent Lecoultre!

We are pleased to announce the arrival of Vincent Lecoultre as a Banker at Cité Gestion.

Read more30.06.2026

Why could the decline in oil prices reshape the investment landscape over the coming months?

La baisse des cours du pétrole pourrait modifier les perspectives d'investissement de multiples façons.

Read more23.06.2026

Crête Equestrian Competition x Cité Gestion

We are proud to have supported the Crête Horse Competition, an exceptional event that brings together passion, excellence, and camaraderie around values that are dear to us.

Read more18.06.2026

Naïma Karamoko x Cité Gestion

Cité Gestion is proud to announce its sponsorship of Naïma Karamoko and to support her promising journey, marked by her recent qualification for the WTA 125 Modena final.

Read more09.06.2026

How much is the SpaceX dream actually worth?

SpaceX’s $1.75 trillion valuation is ultimately a bet that the company can sustain near-flawless execution and technological leadership for 15 years, transforming today’s $20 billion in revenue into $3.4 trillion by 2040—a reflection of how much investors are willing to pay for a bold vision of the future.

Read more04.06.2026

Harvard x Cité Gestion

Cité Gestion was honored to attend the latest Harvard Gala Dinner in Mexico City, celebrating meaningful exchanges among leaders and professionals, while reaffirming its longstanding commitment to fostering dialogue, innovation, and international connections within the Harvard community in Mexico.

Read more